"This is a very serious banking crisis. There's just no question about that," said Donald G. Ogilvie, a longtime president of the American Bankers Association and now a senior adviser at Deloitte LLP.

For much of the past decade, borrowers and lenders have been lulled into a sense of security about the safety of the banking system. As real-estate values soared, banks doled out loans that fed the explosion in residential construction, mortgages and home-equity borrowings. Loan defaults hovered at historic lows as home buyers and builders flipped properties and sold them at huge profits.

At the same time, banks fueled the demand for loans by competing fiercely against one another for customer deposits. They wooed customers with new high-yield savings accounts and certificates of deposit, and special Internet-only promotions. Banks now also routinely encourage customers to pay bills online -- a practice that makes it difficult for customers to sever their banking relationships. And customers who keep multiple accounts at the same bank, such as traditional savings deposits, credit-card accounts or CDs, often get the best rates on loans.

But all too often consumers accumulate money in a single bank to earn better returns or end up exceeding the limits covered by federal insurance simply by not paying attention to a growing balance.

I've touched on this before, but let's return to what the FDIC has said about bank's current conditions:

# INDUSTRY EARNINGS DECLINE 46 PERCENT FROM YEAR-EARLIER LEVEL

# LOSS PROVISIONS ABSORB A HIGHER SHARE OF REVENUE

# TROUBLED LOANS ACCUMULATE IN REAL ESTATE PORTFOLIOS

# LENDING GROWTH SLOWS

# FOURTH QUARTER 2007 EARNINGS ARE REVISED BELOW $1 BILLION

Those are the bullet points at the beginning of the story. None of them are good. Here is the opening paragraph:

Deteriorating asset quality concentrated in real estate loan portfolios continued to take a toll on the earnings performance of many insured institutions in first quarter 2008. Higher loss provisions were the primary reason that industry earnings for the quarter totaled only $19.3 billion, compared to $35.6 billion a year earlier. FDIC-insured commercial banks and savings institutions set aside $37.1 billion in loan-loss provisions during the quarter, more than four times the $9.2 billion set aside in first quarter 2007. Provisions absorbed 24 percent of the industry's net operating revenue (net interest income plus total noninterest income) in the quarter, compared to only 6 percent in the first quarter of 2007. The average return on assets (ROA) was 0.59 percent, falling from 1.20 percent in first quarter 2007. The first quarter's ROA is the second-lowest since fourth quarter 1991. The downward trend in profitability was relatively broad: slightly more than half of all insured institutions (50.4 percent) reported year-over-year declines in quarterly earnings. However, the brunt of the earnings decline was borne by larger institutions. Almost two out of every three institutions with more than $10 billion in assets (62.4 percent) reported lower net income in the first quarter, and four large institutions accounted for more than half of the $16.3-billion decline in industry net income.

Let's take a look at some graphs from the report:

Notice that the amount of money banks are setting aside to absorb losses is increasing, as is the amount of money they are charging off. Neither of these are good developments.

Non-current loan rates are increasing as well

Non-current loan rates and charge offs are also increasing. The non-current loan rate is higher than the highest rate during the last recession. The quarterly net charge off rate is approaching the level it achieved in the last recession.

Non-current rates on residential mortgage loans are increasing

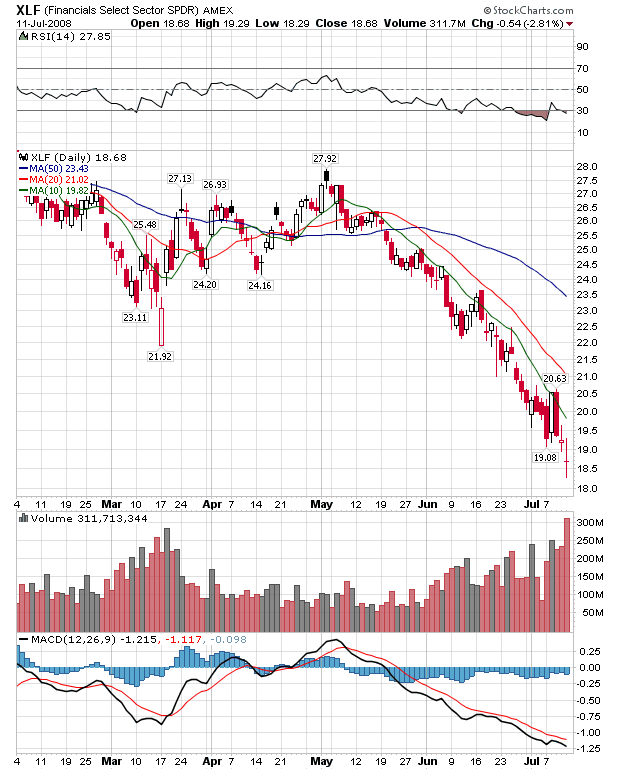

And the charts confirm this problem. Let's take a look at the XLFs which are ETF that tracks the big money firms:

Notice the following:

-- Prices are below all the SMAs

-- The shorter SMAs are below the longer SMAs

-- All the SMAs are headed lower

This is a bear market chart, plain and simple. And it indicates traders are incredibly bearish about the future for financial institutions.

Now - we are not a panic levels by any stretch of the imagination. However, we're also not in a place where we can say "it will all be OK". There is going to be more pain ahead, plain and simple.

No comments:

Post a Comment