One of the big stories for the last 3-6 months is the commodities boom. Just to refresh your memory, the commodity market has been on fire for two inter-related reasons. As the Fed started to cut interest rates it became clear to traders that the Fed was going to let inflation run. As a result, traders bid up commodities as an inflation hedge. In addition, as the Fed cut interest rates the dollar became less attractive as a place to park money, so the dollar continued to fall. Because most commodities are priced in dollars a drop in the dollar is a de facto price gain in anything priced in dollars. So, the commodity and dollar markets were involved in a fairly vicious circle.

The Fed's last rate cut announcement led to speculation the rate cuts were nearing an end. This led to a rally in the dollar and sharp drop in commodity prices last week.

Let's see where the charts stand now:

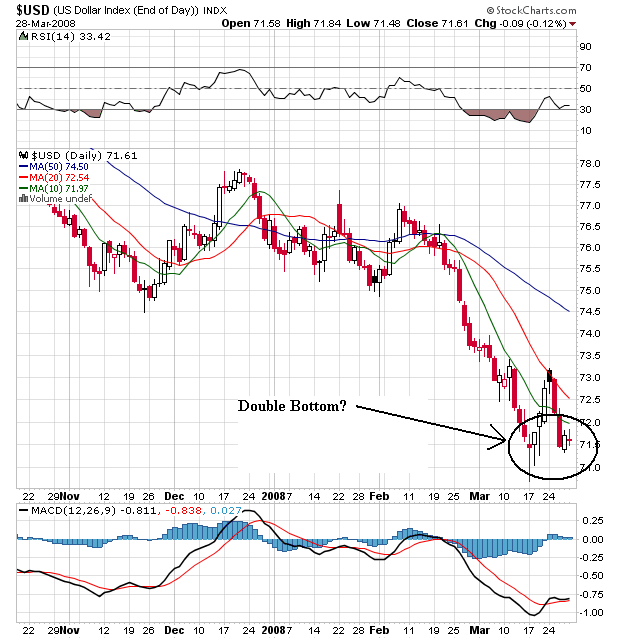

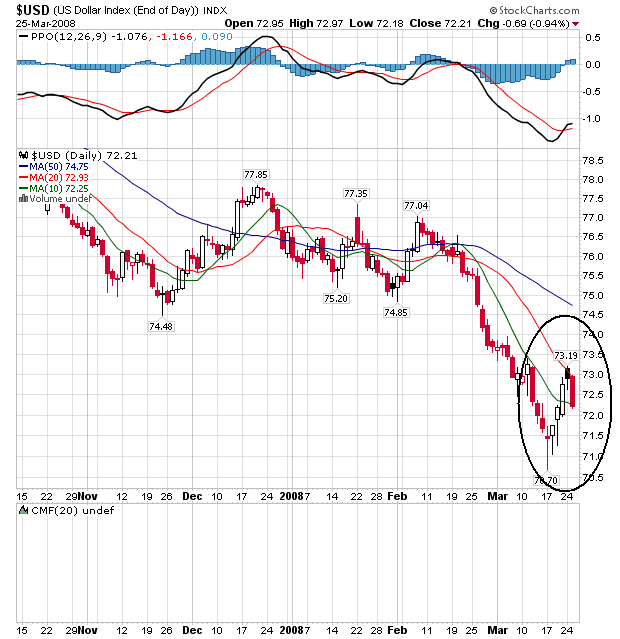

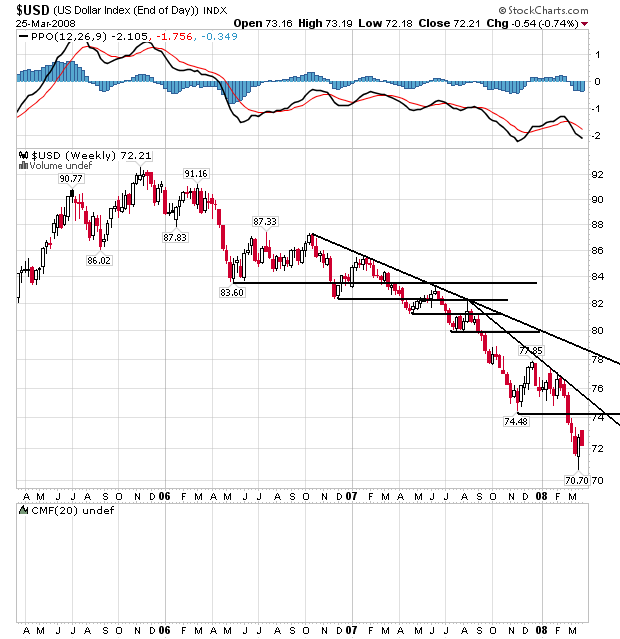

On the dollar chart, notice the following:

-- The dollar rallied to its 20 day SMA and then fell back.

-- The dollar is currently trading at the 10 day SMA.

-- All the SMAs are moving lower

-- The shorter SMAs are below the longer SMAs

The next few days are exceedingly important for the dollar.

On the monthly chart, notice:

-- The dollar is in a clear, multi-year downtrend. It is in a pattern of lower lows and lower highs.

-- The chart has continually broken through technical support.

-- There are several strong downward sloping trends in place.

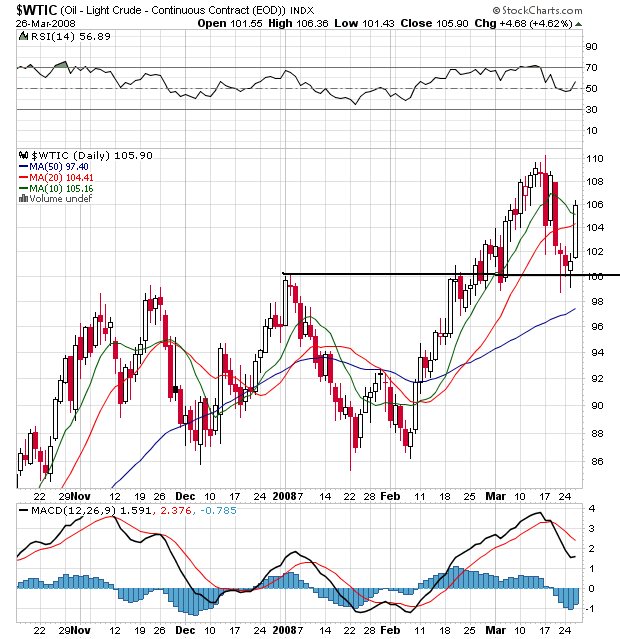

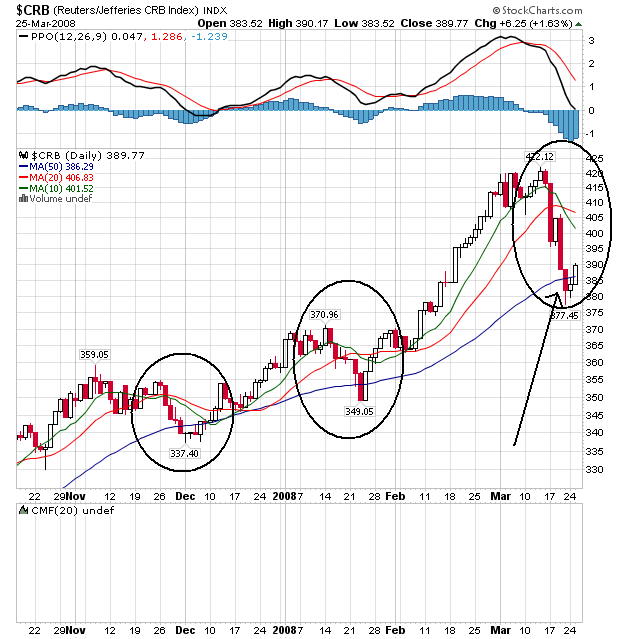

On the commodities chart, notice the following:

-- Two other times in the last 6 months prices have dropped to the 50 day SMA over the period of about a week to a week and a half. Both times prices rallied back.

-- However, the last two times this happened, the SMAs were closer together. Over the last month the 10 and 20 SMA have moved pretty far above the 50 day SMA. In other words, the SMAs might need time to catch-up with price action.

-- Note the 10 day SMA has crossed below the 20 day SMA. This is a bearish crossove and may indicate we have lower prices ahead.

-- So far, prices have repeated what has happened twice before.

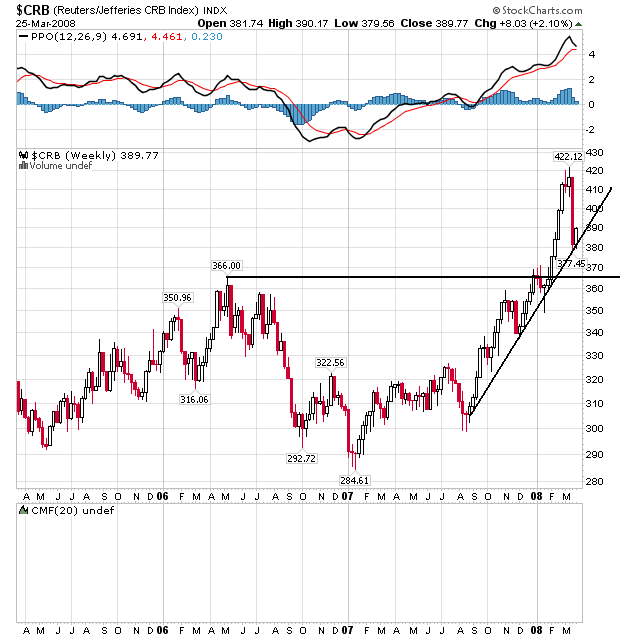

On the monthly CRB chart, notice the following:

-- Prices are currently at the uptrend.

-- There is support at 366 -- about 6% below current price levels.