Yesterday the Federal Reserve released the Beige Book which provides an excellent overview of current economic conditions. So, let's dig in. I'm going to offset the Fed's information and italicize the words.

Despite some variation across Districts, employment levels appeared to be little changed, on balance, from recent months. Some weakening in the job market was reported in the New York, Atlanta, Chicago, St. Louis, and Minneapolis Districts. Cleveland reported flat employment levels, while Richmond indicated mixed trends. Boston and Kansas City indicated modest increases in employment, with some deceleration indicated in the latter. Firms in the Philadelphia, Atlanta, and Minneapolis Districts reported layoffs, reductions in work hours, or hiring freezes in response to current or expected slowing in economic activity.

Above is a graph of establishment job growth. Notice we're just at the beginning of problems in the labor market. In addition, job growth during this expansion has been the weakest of any post WWII expansion. This implies we won't see the same level of lay-offs as we've previously seen in the economy.

Above is a one year chart of employment growth. Notice we're only at the very beginning of a slowdown.

However, as the above your-over-year percentage change indicates, we've been experiencing some problems for some time.

And we're also seeing an uptick in the unemployment rate.

Consumer spending weakened in most, but not all, Districts since the last report. In particular, automobile sales were generally reported to be flat or declining. Vehicle sales were described as unchanged or falling in the Philadelphia, Cleveland, Atlanta, and Dallas Districts and were characterized as weak in the Richmond, Atlanta, Chicago, and San Francisco Districts. However, Kansas City reported that auto sales rebounded in March, though they remained lower than a year earlier. Non-auto retailers reported that sales were sluggish or declining in ten Districts. Elsewhere, Boston noted mixed sales trends, and New York reported a modest pickup since the last report. Chicago, San Francisco, and, to a lesser extent, Philadelphia noted relative strength in demand for luxury goods.

As a result of weak job growth (see above), we've see weak wage growth

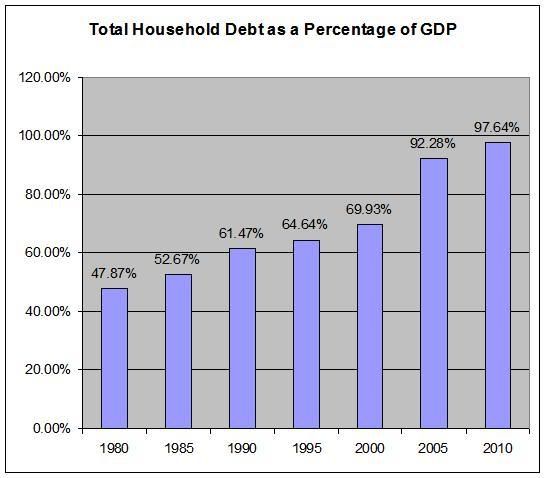

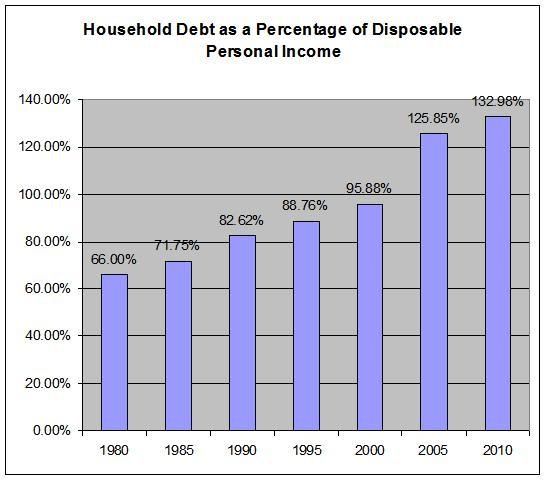

Don't forget the high levels of household debt, which I think have now become enough of a burden to slow spending.

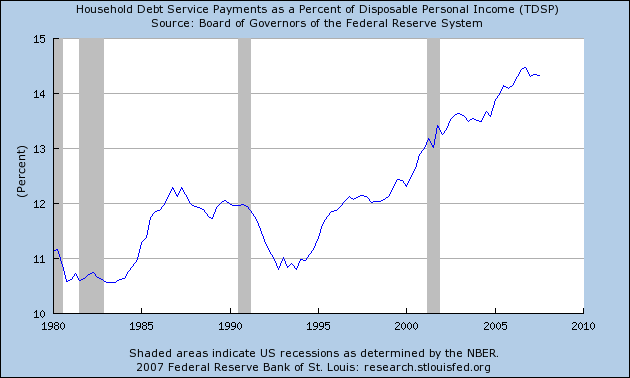

Debt service payments have been increasing for the last few years

All of this leads to declining spending

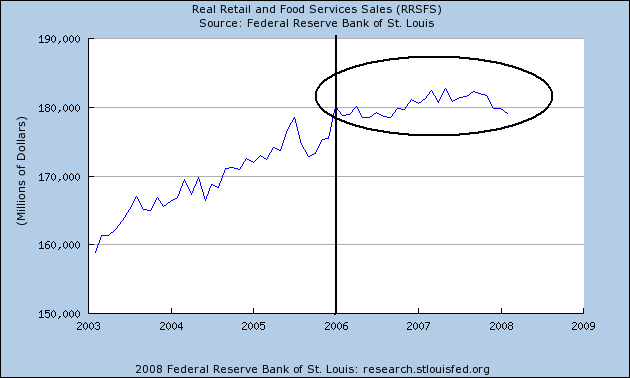

And somewhat stagnant retail sales for the last few years or so

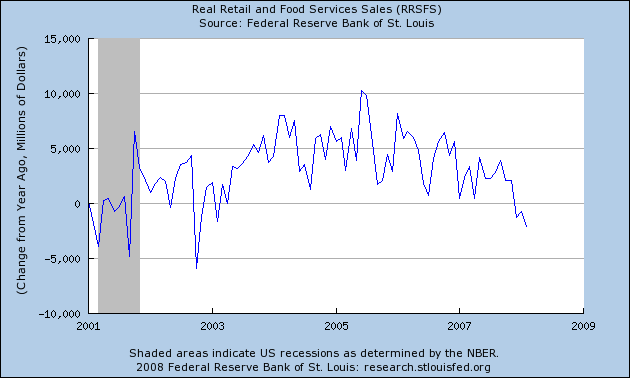

With a declining year over year number

Manufacturing activity was varied, with some Districts reporting a slight increase in activity, some indicating weaker activity, and several noting that activity was mixed or had held steady. Chicago, Boston, and Richmond reported that activity was rising, but not substantially, while New York, Kansas City, Philadelphia and Dallas all reported that activity had weakened. St. Louis and Cleveland said that activity had held steady, while Atlanta, Minneapolis and San Francisco saw activity as mixed.

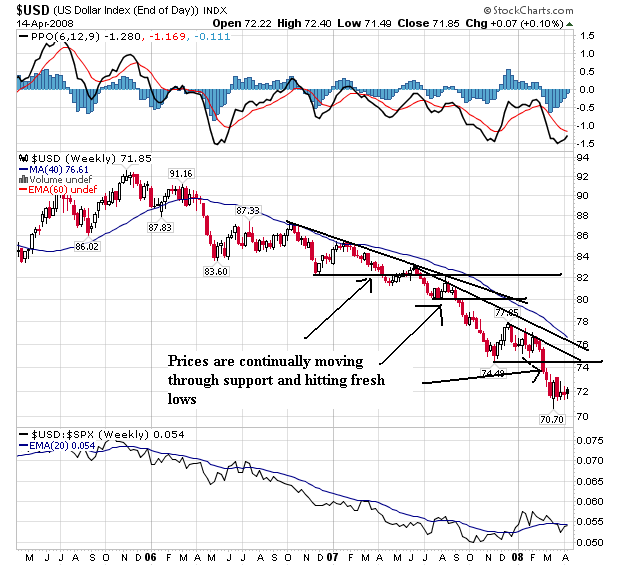

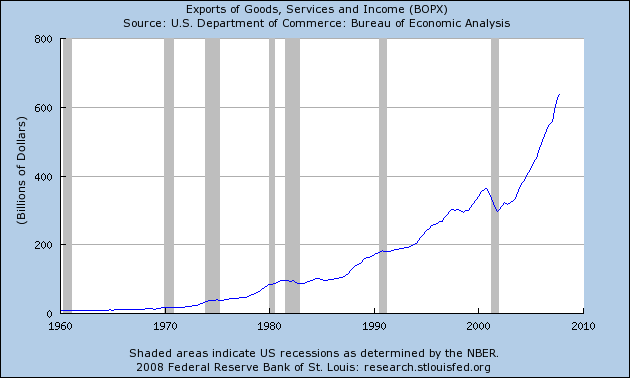

Remember, the main story here is the weaker dollar:

Which has lead to an increase in exports:

But the slumping domestic economy is still hurting manufacturing as shown by the following regional indexes:

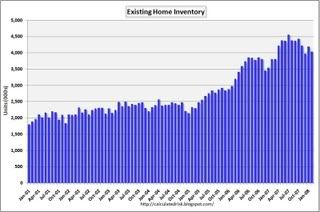

Housing markets and home construction remained sluggish throughout most of the nation, though there were few signs of any quickening in the pace of deterioration. Ongoing weakness in housing markets, in general, was reported in almost all Districts. Sales activity was generally reported to be declining in the Boston, New York, Philadelphia, Atlanta, St. Louis, Minneapolis, Dallas and San Francisco Districts, while Kansas City and Chicago noted slack demand and excess inventories. On the other hand, the Cleveland District saw some pickup in activity, while Richmond and Atlanta reported some pockets of improvement; Boston, Atlanta, and Chicago cited some recent pickup in traffic or buyer inquiries. New residential construction was reported to have remained at depressed levels, and none of the Districts reported any pickup since the last report.

First, there is a ton of inventory on the market. Here is a chart of total existing inventory from Calculated Risk

Notice in the story above economists were predicting 750,000 to 1 million more homes will hit the market in the next year as a result of the increase in foreclosures. That means at minimum we'll see no meaningful drop in inventory over the next year.

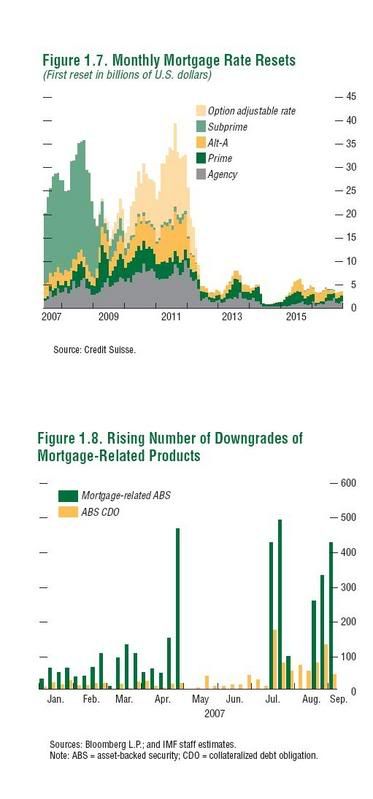

And here is a chart from CSFB that shows we're nowhere near the end of foreclosures related to changing mortgage terms. In fact, we have a second wave to go through in about a year and a half:

At the same time, the US consumer is in debt up to his eyeballs and can't afford to talk out much more debt.

So -- there is little reason to think inventory will decrease in the coming year and there is little reason to think people will rush into the housing market because they are already under a tremendous amount of debt.

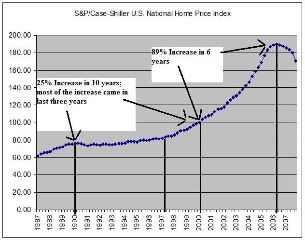

So -- what does that mean for prices? If inventory isn't decreasing and fewer people are able to take out a loan that means prices will have to drop. And considering how out-of-whack home prices are anyway, that shouldn't be much of a surprise:

Compare the 1990s with the 2000s (but also remember we were working on another bubble in the 1990s). Despite the fact that things were good in the 1990 we didn't see a huge increase in prices. However, we made up for lost time in the 2000s. Simply put, prices are going to drop before they move higher.

Business contacts across all Districts continued to report increases in input costs and output prices. In particular, price increases were consistently reported for food products, fuel and energy products, and many raw materials. More specifically, increases in the price of chemicals, metals, plastics and other petroleum-based products were commonly cited. Most manufacturers have or are planning to increase prices in response to rising input costs, while the response of service firms has been more mixed, in part due to differences in competitive pressures. On balance, input costs have risen more rapidly than output prices, putting pressure on margins for many firms. Most Districts reported little change in retail price inflation, though Richmond and San Francisco noted some moderation. Most business contacts reported that wages were unchanged or were increasing moderately in all Districts. Business contacts in the Atlanta, Chicago, Cleveland, Dallas, Philadelphia, and San Francisco Districts indicated that there has been some upward wage pressure for skilled labor in some sectors that continue to experience shortages.

For anyone who reads my blog on a regular basis, you should know that inflation is nowhere near under control. Here's one example and here's another example.

However, for those of you who have forgotten, here are the relevant year-over-year charts.

So -- the short version is the economy is slowing and inflation is rising. Not a good combination.

Charts from Econoday

{kind=link}

No comments:

Post a Comment