Almost one-third of U.S. homeowners who bought in the last five years now owe more on their mortgages than their properties are worth, according to Zillow.com, an Internet provider of home valuations.

Second-quarter home prices fell 9.9 percent from a year earlier, giving 29 percent of owners negative equity, said Zillow, the Seattle-based service that offers values for more than 80 million homes. For those who bought at the 2006 peak of the housing market, 45 percent are now underwater, Zillow said.

Let's think about that for a minute, shall we? 1/3 of the all the mortgages originated in the last five years in the US are larger than the value of the homes they are tied to. According to the Federal Reserve's Flow of Funds Report total mortgage debt outstanding in the first quarter of 2008 was $10.6 trillion and total mortgage debt outstanding in the 1Q 2003 was $6.222 trillion. So over the last 5 years we've see an increase of $4.3 trillion in mortgage debt. Let's assume that 25% of that is home equity, leaving us with $3.321 trillion in first lien mortgages. That means $1.086 trillion of mortgages are more expensive than the properties they are tied to. That's also roughly 10% of all mortgages in the US financial system.

Let's add to the analysis.

Home foreclosure filings rose 14 percent in the second quarter, the eighth consecutive quarterly climb, and more than doubled from the same period a year-earlier, real estate data firm RealtyTrac said on Friday.

Home foreclosure filings during the second quarter were reported on 739,714 U.S. properties, up 121 percent from a year earlier, RealtyTrac, an online market of foreclosure properties, said in a report.

The figure is a total of default notices, auction sale notices and bank repossessions between April and June.

We've seen two straight years of increases in foreclosures and a doubling (as in times two) of the foreclosure rate from last year. That's a mammoth increase. Putting that together with the number of homeowners who are underwater we get a really scary picture.

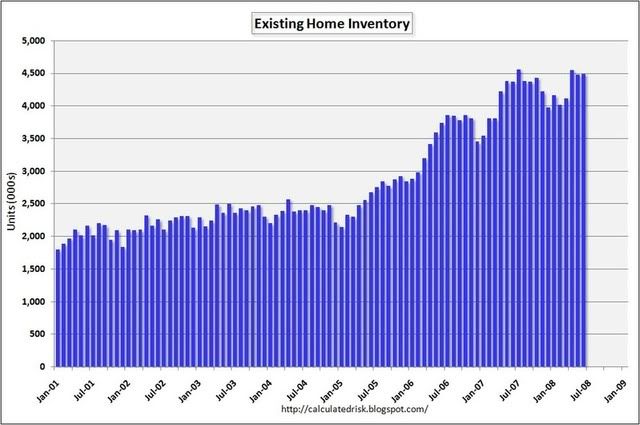

As those foreclosures increase we'll see an increase in existing homes for sale inventory (chart from Calculated Risk):

And who is going to buy these houses with Credit getting tighter -- at least according to the Federal Reserve's latest survey of lenders:

Large majorities of domestic respondents reported having tightened their lending standards on prime, nontraditional, and subprime residential mortgages over the previous three months. About 75 percent of domestic respondents—up from about 60 percent in the previous survey—indicated that they had tightened their lending standards on prime mortgages.2 Of the 32 respondents that originated nontraditional residential mortgage loans, about 85 percent—up from about 75 percent in the April survey—reported having tightened their lending standards on such loans.3 Finally, 6 of the 7 respondents that originated subprime mortgage loans—a somewhat higher proportion than in the April survey—indicated that they had tightened their lending standards on those loans over the past three months.4

Let's also note the US families are massively indebted. Total household debt outstanding is now $13.9 trillion.

All of this activity -- homes underwater, increasing foreclosures, tightening credit -- is leading to an increasing rate of home price declines:

Prices of U.S. single-family homes plunged at a record pace in May from a year earlier, with each of the 20 regions monitored showing annual declines for a second month, according to the Standard & Poor's/Case Shiller home price indexes reported on Tuesday.

A lot of this is a chicken and egg situations -- are foreclosures leading to price declines, or are price declines leading to increasing foreclosures? At this point it doesn't matter. The bottom line is there are some serious problems in the housing market and there aren't any signs it is ending soon.

No comments:

Post a Comment